The Massive Valuation Gap the Market is Missing: Why Energy is a High-Conviction Trade

- Jun 24

- 3 min read

The market is presenting a massive structural anomaly as U.S. Energy equities trade lower than their pre-war levels despite severe geopolitical supply disruptions. While capital remains heavily concentrated in high-multiple tech names, the energy sector is experiencing a massive fundamental upgrade, highlighted by an $78 billion surge in free cash flow across just five top producers and refiners. With global stockpiles depleted and a rotation into tangible, heavy assets underway, this valuation gap offers an incredibly asymmetric risk-reward profile.

In quantitative trading, our edge lives in stark fundamental disconnects. Right now, a massive divergence is playing out between soaring geopolitical risk, surging cash flows, and lagging energy equity valuations. While the broader market remains hyper-focused on tech multiples, the physical world is signaling a massive structural shift. Here is why physical infrastructure is looking like an incredibly clean risk-reward trade right now.

The Glaring Market Disconnect

Despite severe disruptions to oil and natural gas shipments through vital choke points like the Strait of Hormuz, U.S. energy stocks are behaving counterintuitively. The index of U.S. energy companies is trading lower than it was before the conflict, lagging technology by a mile.

To put this structural undervaluation into perspective: the entire U.S. energy sector is worth only half as much as Nvidia alone. Furthermore, the three largest energy producers combined have a lower market value than Micron.

The market is entirely missing how long elevated commodity prices are likely to remain high. Unlike the speculative assumptions built into tech growth, the near-term cash flows of energy stocks are tangible, defensive, and remarkably easy to quantify.

A $78 Billion Free Cash Flow Windfall

When you look past the price charts and dive into the revised analyst consensus forecasts for 2026 and 2027, the structural cash generation is staggering:

The Producers: For the three largest players (Exxon Mobil, Chevron, and ConocoPhillips), combined free cash flow expectations have jumped by $60 billion.

The Refiners: For the two dominant refiners (Valero and Marathon), FCF expectations are up by $18 billion.

Across just these five core companies, the market is looking at a 53% increase in distributable cash.

Why the Tailwinds Are Structural (Not Just Cyclical)

Typically, energy booms sow the seeds of their own destruction via aggressive CapEx spending. But this time is different:

No CapEx Overhang (Yet): The current crisis hasn't lasted long enough to trigger a ruinous wave of oversupply or structural demand destruction.

Depleted Global Stockpiles: Both private and government stockpiles of oil and refined products have been heavily depleted globally, guaranteeing a mandatory restocking cycle and a firm floor for extra demand.

The Western Hemisphere Premium: Customers are no longer viewing every supplier equally. Reserves and infrastructure located in politically stable regions far from active war zones are poised to command a structural stock-market premium.

Trading the HALO Rotation: My Take

Before the conflict, institutional capital began rotating into what has been dubbed the HALO (Heavy Assets, Low Obsolescence) trade. This rotation ripped through U.S. stocks precisely when it became clear that geopolitical turmoil could easily disrupt once-high-flying, intangible knowledge businesses like software.

From a trading perspective, the setup here is incredibly asymmetric:

The Edge: In a multi-platform environment, running a quantitative scanner or a pairs trading model on these large-cap energy names vs. overextended tech names reveals a massive divergence. When a sector's FCF jumps by 53% while its equity price drops, the underlying valuation compression creates a spring-loaded setup.

The Strategy: Look to capture this fundamental disconnect by building long exposure in Western-hemisphere producers and refiners (like Exxon or Marathon) that are generating immediate, un-obsolescent cash flows. This isn't a trade based on speculative growth five years out; it's a structural value play backed by immediate, tangible cash yield.

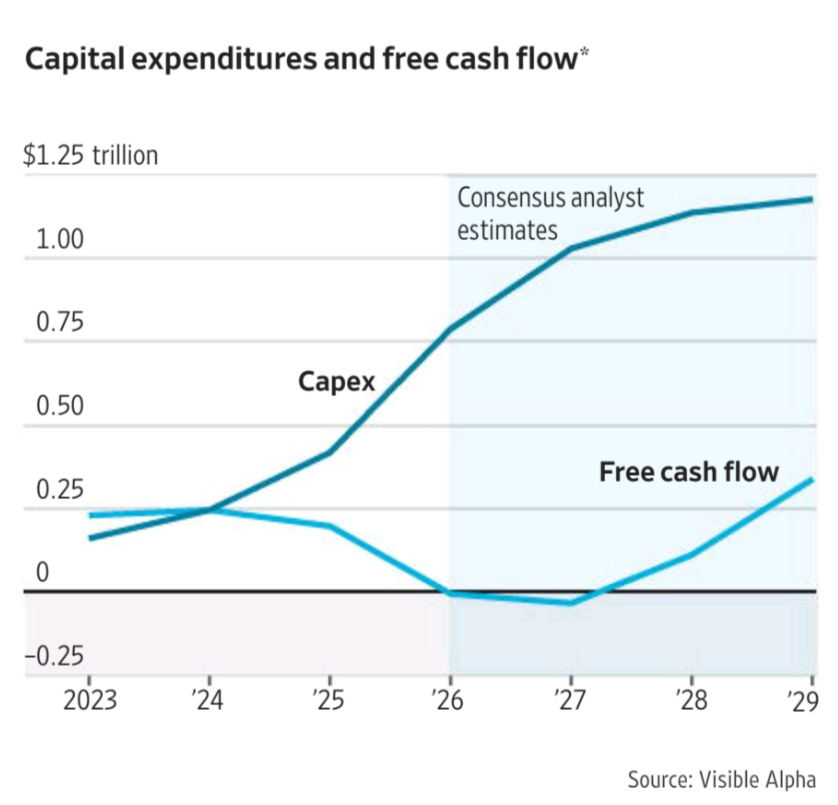

Chart from WSJ

Comments